I pay all my bills on time and don’t have any debt; I’m okay, right?

When you combine a high income with some foundational money management skills, it feels great. Money doesn’t feel as tight, and dreams start to become a reality.

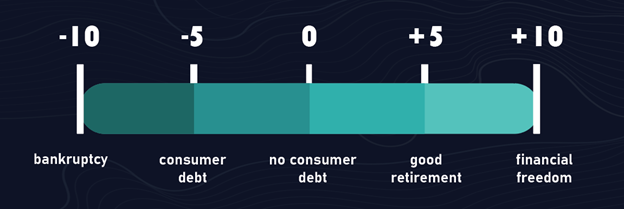

Unfortunately, it’s not always easy to stay on track. With so many people in debt, living paycheque-to-paycheque or worse, it’s easy to see getting out of debt and having money at the end of the month as the end goal. I don’t share that opinion. Think of it this way; your finances are on a scale ranging from -10 to +10. On -10, you have bankruptcy, and +10 you have complete financial freedom, the ability to live life the way you want without financial constraints. 0 is where you enter this world—you don’t owe any money and don’t have any money.

Many of us start our adult life below 0, typically due to student loans. From here, people make choices—either continue to go negative or pay off debt and begin to accumulate money. Assuming you choose to accumulate, you will find yourself consumer debt-free (aside from a mortgage). Congratulations, you are now back at 0. Now what? This is where people get comfortable. There are no immediate consequences for spending since you have plenty of disposable income; you pay off your credit cards each month and treat your friends and family. Things are good.

You may ask, “why would I still track my expenses?”

You shouldn’t; most won’t do anything with the information they gather while tracking anyway. My biggest problem with tracking your expenses is it’s reactionary. To achieve big goals, you must be proactive. “I will spend no more than $100 on this item” is very different from saying, “I spent $70 on this item.” One indicates a plan; the other is reacting to what’s already happened.

If you have significant financial goals, you won’t reach them by being reactionary—you must take control and drive the ship. Instead of tracking what you spent, try setting what you are going to spend. Do this for the week, then the month, and eventually, you’ll be able to do it for the whole year. Setting your expenses helps you achieve four core things:

1. Avoid lifestyle inflation

2. Empowers you to make decisions regarding your financial trajectory

3. Teaches you to be intentional with your resources

4. Creates consistency and discipline

All these things are needed if you want to achieve major goals like financial freedom. Being “good” with money but living reactionary with finances can get you to 5 on the scale. To get further, however, you must be proactive.

What is your first step?

Being proactive is harder; it’s more natural to be reactive. So make a plan, on paper and share it with a loved one.

If you have a goal to lose weight, what’s going to be more productive—eating for the week and then counting up the calories at the end? Or setting a meal plan, knowing what you’re going to consume during that week before the week even starts?

Don’t track expenses, be intentional, and set them.